Identity comes before credit

Business identity fraud doesn’t beat the credit score — it chooses what the score sees. Why KYB and identity verification come before credit checks, and the three identity questions.

Business identity fraud doesn’t beat the credit score — it chooses what the score sees. Why KYB and identity verification come before credit checks, and the three identity questions.

Credit exposure can grow while sales stay flat. The Two Books framework: why commercial dashboards hide the debtor book, and how merchants should monitor credit exposure.

Trade credit is unsecured business lending. Every supplier extending payment terms runs a loan book — here’s how to manage the debtor book like the lending portfolio it already is.

The constraint on UK B2B credit just moved: capital is no longer the limit on lending — underwriting judgment is.

Approval feels like the decision. It’s actually the moment you know least about what happens next. Every credit process treats approval as the decision. You run the check, you approve or decline, you move on. But approval is the moment you know the customer best and your exposure to

This week's UK B2B credit signal: credit supply is loosening while receivables risk is rising.

Two customers, same sector, same limit request. One is strengthening, one is weakening — and the sector view gives you one answer for both. Two customers sit in the same sector and ask for the same limit. One is strengthening. One is weakening. The sector view gives you the same answer

The email arrives on a Tuesday. Your trade-credit insurer has reduced the cover on one of your larger customers — a wholesaler you have shipped to for three years without a missed beat. Nothing has defaulted. There is no county court judgment, no news, no obvious reason. Just a number

UK B2B credit and lending news digest, 21–27 June 2026 Summary UK private-sector activity tipped into contraction this week. The flash S&P Global UK Services PMI fell to 48.7 in June from 49.3 in May — a second straight month below 50 and the steepest

Two suppliers extend credit to the same building contractor. Same trade, same region, same credit score sitting quietly at the top of both their files. One of them shortens terms in early May and caps the exposure. The other keeps shipping on thirty-day terms until a winding-up petition

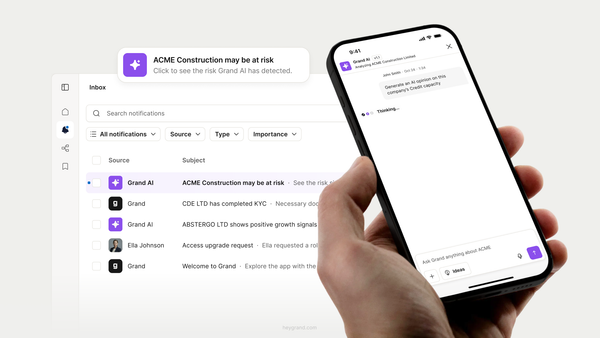

Every credit decision asks three questions. Most tools only answer one—and we keep letting them answer all three. Think about the account that went wrong. Not the one that failed a check — the one that sailed through it. The report came back low risk. Clean score, green light. You

CCJs, winding-up petitions, director changes and late filings rarely arrive without warning. The question is whether you see them in time to act. Two builders’ merchants supply the same contractor on the same 60-day terms. Same invoices, same exposure. When the contractor goes under, one merchant has been

UK B2B credit and lending news digest, 7–13 June 2026 Summary New this week: UK monthly GDP turned negative for the first time since August 2025, contracting 0.1% in April as the Middle East conflict fed through to services output.(1)(2) What matters isn't the

Thoughts

For most credit controllers, the aged debt report is still the starting point for the day. It shows what is overdue, how long it has been overdue, and where the biggest balances sit. But aged debt only tells you what has already happened. For experienced credit controllers, especially those managing

News

UK B2B credit and lending news digest, 17–23 May 2026 Opening Summary The British Business Bank confirmed a £350m ENABLE Guarantee with Allica Bank, including Sona Asset Management as another investor, to unlock up to £700m of SME asset-finance lending.¹ This is the week’s clearest credit-supply

News

UK B2B Credit and Lending News Digest 10–16 May 2026 – Covering 10–16 May 2026. Summary Funding Circle’s 2025 Economic Impact Report, produced with Oxford Economics, confirmed that alternative providers and challenger banks now account for 68% of UK SME lending, making the Big Four the structural minority.

Thoughts

Checking credit risk is like checking the structural health of a bridge before sending heavy trucks across it. The bridge may still be open, but you need to know if cracks are forming, whether the load is getting heavier, and when it is time to slow down, reroute, or stop

Thoughts

For decades, commercial credit assessment has suffered from the same fundamental problem. Most decisions are made using static snapshots of businesses that are constantly changing. Financial statements are outdated by the time they are filed. Credit reports often miss operational deterioration. Manual reviews depend heavily on fragmented data, analyst interpretation,

News

UK B2B Credit Intelligence Digest — 3–9 May 2026 Summary The Construction Products Association cut its UK construction forecast to −2.5% for 2026, its biggest single downgrade on record, and the April construction PMI collapsed to 39.7 (from 45.6 in March). Two things to watch underneath the

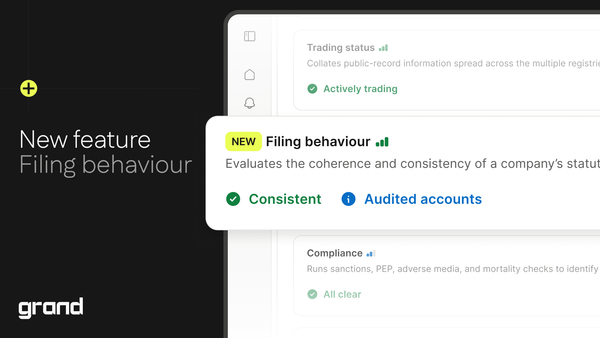

Product

There's a question that shaped everything we built over the last year. What if AI's role in credit isn't to make the decision, but to help the person making it understand what's changing before it's too late? That question led

Thoughts

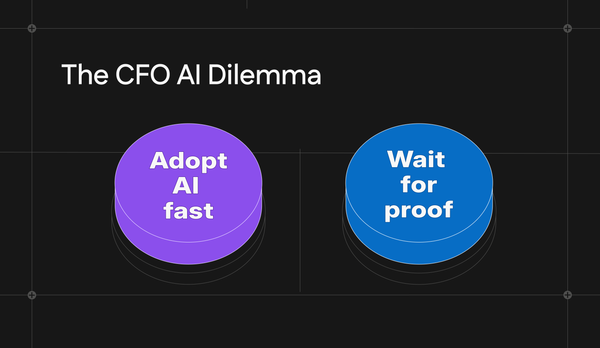

There's an old saying in business. What gets measured gets managed. But today, UK CFOs are discovering a harder truth. What doesn't get automated gets left behind. Across British boardrooms, the pressure to adopt artificial intelligence has stopped being a strategic conversation and started being a

News

Risk moves off bank balance sheets — toward directors, suppliers and specialist finance — Covering 19–25 April 2026 · Published Tuesday 28 April 2026 Summary This week’s credit signal is fragmentation, not uniform tightening. Banks are still competing on mortgage pricing, while SME risk is surfacing through director guarantees, supplier payment

Product

One thing we keep hearing from partners is just how fast we ship new stuff. We assumed, from years of building, that this was normal. It’s not. They’re used to incumbents moving in rigid cycles. A new product every few years. A feature release once a year. The

Thoughts

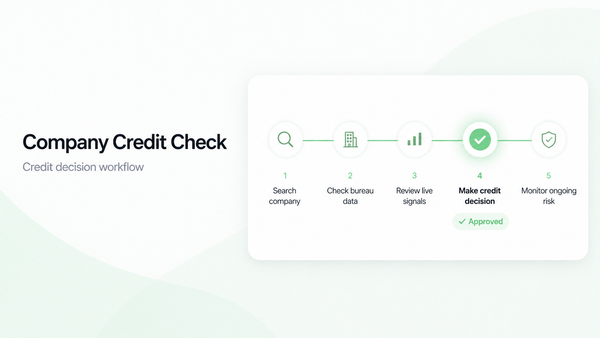

Running a company credit check once is like checking the weather the morning before a week-long sailing trip. Useful but not the same as watching the forecast every day. But most businesses are running them at the wrong moment, reading them the wrong way, and treating a single report